NOV’s two segments are going in different directions. The real story is about what this means for the future of OFS.

CEO Jose Bayardo summed it up near the top of the company’s 2025 Q4 earnings press release:

===

Our Energy Equipment segment posted its fourth consecutive year of revenue growth and EBITDA margin expansion…This performance largely offset a four percent revenue decline in our shorter-cycle Energy Products and Services segment…

===

📈 What’s driving the divergence?

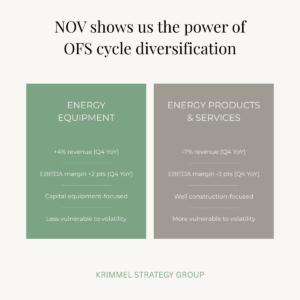

➤ Energy Equipment designs, builds, and supports the heavy equipment at the center of oil & gas operations: drilling rigs, hydraulic fracturing and coiled tubing spreads, cranes, separators, subsea pipe, pumps, heat exchangers, and more.

➤ Energy Products and Services provides downhole tools and services: drill bits, motors, MWD and LWD tools, frac plugs and sleeves, ESPs, drill pipe coating and inspection, solids controls, MPD, and more.

Energy Equipment grew 4% year-over-year in Q4.

Growth came not from surging activity, but from executing on a $4.3 billion backlog of long-cycle offshore production projects.

Subsea flexible pipe hit record revenue. Process systems and marine construction are also driving growth.

These businesses provide visibility and insulation from quarter-to-quarter drilling activity swings.

Energy Products and Services is more exposed to short-cycle drilling and completion activity.

When rig counts decline (as they did in 2025 in North America, Saudi Arabia, and Argentina), this segment feels it immediately.

Even market share gains couldn’t fully offset the activity headwinds.

🔎 Why does this matter beyond NOV?

There is an increasingly accepted principle in oilfield services: you have to diversify beyond short-cycle well construction.

NOV already had the portfolio.

SLB pursued the ChampionX acquisition for production chemicals exposure, downstream of well construction.

Halliburton is increasingly focused on international and deepwater markets where projects are larger and less volatile.

In a world where oil price volatility is likely to increase, oilfield service companies are looking to diversify in ways that stabilize cash generation.

E&P consolidation is about scale within the same business model.

OFS diversification is about cycle exposure: reducing dependence on short-cycle drilling activity by pursuing long-cycle international and offshore projects, and by gaining more exposure to production.

It’s not simply about being in more markets. It’s about being in markets with different timing and volatility profiles.