Devon is 73% liquids. Coterra is 65% gas. Together, they’re building something neither could create alone.

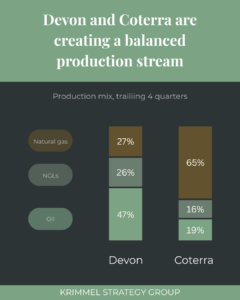

Devon has a notable focus on liquids. 73% of its production stream is comprised of oil and natural gas liquids (NGLs).

Coterra brings the gas, with only a third of its production as liquids.

In a market that is notoriously volatile and is in the process of bifurcating, this optionality matters.

Legacy Devon picks up the gas exposure that investors want, given the growth in power demand and continued LNG export infrastructure buildout.

Legacy Coterra picks up the powerful economics of the liquids side.

Remember that on an energy-equivalent basis, it takes 6 thousand cubic feet of natural gas to equal one barrel of oil.

Even if gas prices are $5 per thousand cubic feet, that’s an oil price of $30 per barrel.

The oil economics are strong, even as the attention of the market snaps hard to natural gas.

The combined company has the bedrock economics of liquids that can fund aggressive cash returns to shareholders, but also the gas exposure to partake meaningfully in the enthusiasm around gas.

I spoke at the Petroleum Club a couple of weeks ago about strategic optionality in the oilfield.

This deal is a classic example.

Now that another consolidation domino has fallen, what do you think the next deal is?