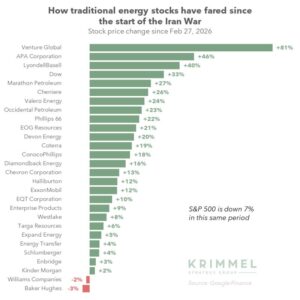

The S&P 500 is down 7% since the start of the Iran War. But 26 of 28 large traditional energy stocks I follow are up over the past month.

The chart below shows the companies I’m talking about.

Venture Global, the LNG producer, is at the top of the list, with its stock up 80% since the war started.

That’s not a huge surprise, given that Venture Global has more exposure to the spot market than its peers, and spot LNG prices have shot up.

Qatar is a major global LNG producer. They brought production offline as the war started, and then some of their critical infrastructure was damaged, requiring years-long repairs.

US LNG producers gained with the market having to turn elsewhere for supply.

The very bottom of the list is Baker Hughes, which has at least three elements working against it at the moment:

➔ Its oilfield service business has considerable activity in the Middle East, which may not quickly recover

➔ Its portfolio has a considerable industrial component that doesn’t benefit from rising oil and gas prices the way its oilfield service business could

➔ Its debt-heavy acquisition of Chart Industries is still pending, and if interest rates rise as a result of oil price spikes, the company’s debt burden will get heavier

As you linger near the bottom of the list, you’ll find midstream players like Williams, Kinder Morgan, and Enbridge.

This positioning is more about the commercial reality of the midstream space.

There’s less upside for midstream companies as commodity prices spike.

Crude producers would benefit from higher sales prices. Refiners may benefit if spreads between finished product and crude prices widen.

But midstream doesn’t have the same exposure.

And the energy cost for processing and transportation goes up with war-driven disruptions.

We see APA catching a break here, continuing its recovery from a real walloping that started after last year’s Liberation Day tariff announcements.

Plus, they have a presence in Egypt that may become more strategically important with ongoing Middle East conflict.

The chemicals companies are also finding new life, with supply disruptions helping cure a structural imbalance that had plagued that sector for the past few years.

And E&Ps are mostly clustered in the 10-20% range, reflecting the broad oil price uplift without any company-specific catalysts.

There is a pair of questions that the investors piling into these stocks are now trying to answer.

Are today’s energy market distortions temporary, and thus will be unwound quickly once combat subsides?

Or are these dislocations enduring, and we should thus expect structural changes in the years ahead?