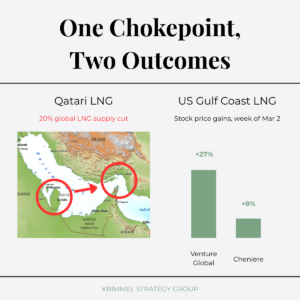

Qatar shut down its entire gas liquefaction operation. That’s 20% of global LNG offline, which has real impact for US producers.

According to Reuters, Qatar Energy has fully shut down gas liquefaction after the outbreak of combat in Iran, and doesn’t plan to restart for at least two weeks.

Then when liquefaction does restart, it’ll take two more weeks to get back to full capacity.

Four weeks without that supply will lead to price increases globally, which we’re already seeing.

In the past week, Dutch TTF futures are up over 60%. JKM LNG prices are up over 40%.

Unsurprisingly, Venture Global’s stock is up nearly 30%, and Cheniere’s is up nearly 10%.

Venture Global’s stock is up so much in part because it has more uncontracted LNG cargoes than most of its peers.

In a supply crunch, spot exposure is an advantage.

Cheniere’s upside is structural rather than immediate. If global buyers start shifting long-term contracts toward US suppliers, Cheniere wins.

This is part of the calculus of building LNG infrastructure along the US Gulf Coast.

Qatar’s resources are world-class. Its costs are among the lowest anywhere.

But every cargo has to pass through the Strait of Hormuz.

That single chokepoint means the economics of Qatari LNG carry a vulnerability that doesn’t show up in other regions.

US facilities, for example, don’t share that exposure.

The US Gulf Coast export corridor faces its own risks, e.g. hurricanes, permitting timelines, and infrastructure bottlenecks.

But as a developer, you don’t assume the risk that a regional military conflict shuts down your entire operation overnight.

There’s been an ongoing debate about whether US developers are building too much LNG capacity.

This week is a reminder that the “right” amount of capacity depends heavily on assumptions about geopolitical stability that can change in hours.

The harder question is what happens when Qatar comes back online.

If this disruption is measured in weeks, it’s a short-term price spike that does not fundamentally remake the fortunes of US producers.

If the Strait of Hormuz remains contested for months, it’s a structural repricing of where the world sources its LNG. And that repricing favors the US.