So far in 2026, Targa’s stock is up 26%. The S&P 500? Flat. And buybacks are an important part of the story.

Last week Targa Resources, the $50B market cap midstream giant, reported its 2025 earnings results.

One thing that stood out?

How well it repurchased its own stock.

In 2025, Targa repurchased nearly 2% of its outstanding shares for around $640 million.

2% may not sound like much. But that’s a serious commitment of capital, helping to boost the ownership stake of every existing shareholder in the process.

It’s not just the scale of the buyback.

It’s how well executed it was price-wise.

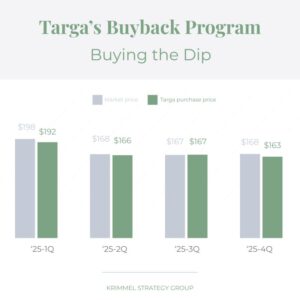

📊 As we see in the chart below, Targa’s average repurchase price was below the average market price in three of the four quarters of the year.

Across the whole year, Targa’s average repurchase price was 2.6% below its average stock price, meaning the company did well buying at a relatively attractive prices.

➤ In Q1, its stock price averaged $198. Targa spent $125 million in buybacks.

➤ In Q2, its stock price dropped 15% to $168. Targa ramped its buyback spend up 160%, deploying $324 million to repurchase shares.

Many companies don’t do that.

They have a set amount of cash to spend on buybacks, and they spend it more or less evenly, insensitive to what its stock price is doing.

Targa’s management clearly had an intrinsic value in mind.

When Q2 hit and the stock price dipped below it, the company turned the dial up and vacuumed up a lot more shares.

Buybacks can generate negativity through charges of unfair financial engineering.

But when used well, they can create incredible value for the remaining shareholders.

At low enough prices, management is essentially buying their own future cash flows at a discount, sometimes the best investment available to them.

🔎 The 2025 results are a useful case study in what sophisticated capital allocation actually looks like in practice.

It’s not just returning cash to shareholders, but timing that return against a view of what the company is worth.